The CTV Media Market

Executive Summary

Connected TV (CTV) has evolved beyond a simple extension of linear television—it is now the central nervous system of video content distribution and advertising. For media companies, advertisers, and telcos alike, understanding the structural dynamics of the CTV ecosystem has moved from "nice-to-know" to "strategic imperative."

This whitepaper synthesizes the latest Q1 2026 market research to address three core questions:

- 1. Market Landscape: Who leads the US and global CTV markets, and why the distinction between smart TV OS share and total device share matters.

- 2. Distribution Strategy: Why OS-level presence has become the primary determinant of discoverability, engagement, and monetization—and how different levers (pre-installs, premium placement, remote buttons, deep linking) drive incremental lift.

- 3. Advertising Economics: How the $44.7B global CTV ad market is structured, where value accrues, and what CPM trends mean for advertisers and publishers.

Key conclusions:

- Roku leads total CTV device share (28%) in the US, while Samsung (Tizen) leads smart TV OS share (34%). Distribution strategy must account for this split.

- Premium app-row placement drives the largest incremental lift in MAUs (80-120%), while deep linking and OS-level content merchandising drive the highest paid conversion lift (30-50%).

- The CTV ad market is growing rapidly but becoming a buyer's market: CPMs are under pressure, programmatic share is rising, and value is concentrated among OS platforms and OEMs—not publishers.

Market Overview: Global and US CTV Landscape

Global Market Dynamics

The Connected TV (CTV) ecosystem has evolved into a globally scaled, platform-driven market, with regional dynamics shaped by device penetration, broadband infrastructure, and platform dominance.

🌍 APAC: The Growth Engine of Global CTV

The Asia-Pacific (APAC) region has emerged as the largest and fastest-growing CTV market globally, accounting for 38.57% of total CTV revenue in 2024, with a projected CAGR of 14.4%—the highest among all regions.

Key Drivers of APAC Growth:

- Rapid Smart TV Penetration: Strong growth in mid-range and affordable smart TVs (TCL, Xiaomi, Hisense); increasing adoption in price-sensitive markets like India and Southeast Asia.

- Mobile-First to TV Migration: Users transitioning from mobile video consumption → large-screen viewing; CTV becoming the primary household entertainment hub.

- OS Fragmentation with OEM Control: Multiple OS ecosystems (Android TV, VIDAA, PatchWall, Tizen); strong influence of OEM-led platforms; lower platform concentration, higher complexity for advertisers.

- Ad-Supported Growth (AVOD/FAST): Price sensitivity drives free, ad-supported streaming models; rapid expansion of FAST channels.

🌎 North America: The Most Mature & Monetized Market

While APAC leads in growth, North America (especially the US) remains the most mature and monetized CTV market globally.

- Platform Consolidation: Dominated by Roku, Amazon Fire TV, Samsung Tizen → high bargaining power at OS level, concentration of advertising value.

- Advanced Programmatic Ecosystem: ~45-55% of CTV transactions are programmatic; strong adoption of PMPs and data-driven targeting.

- High ARPU & Ad Spend: Higher ad loads and CPMs vs global markets; CTV is now a core channel in media planning.

🌍 Europe: Fragmented but Regulated Growth

Europe represents a mid-maturity market, with growth constrained by GDPR, fragmented language and content ecosystems. Strong public broadcasters transitioning to CTV, slower programmatic adoption, increasing focus on privacy-compliant targeting.

1. Growth vs Monetization Split: APAC = Scale + Growth; US = Monetization + Control. Global players must balance volume markets (APAC) with high-yield markets (US).

2. OS Layer Determines Market Power: US → platform-controlled ecosystem; APAC → OEM + fragmented OS. Degree of OS consolidation directly impacts who captures value.

3. Advertising Models Diverge by Region: APAC → AVOD/FAST driven; US → Programmatic + premium inventory. Monetization strategies must be region-specific.

4. The Convergence Trend: All markets moving toward platform-led discovery, content-level targeting, and OS-level monetization.

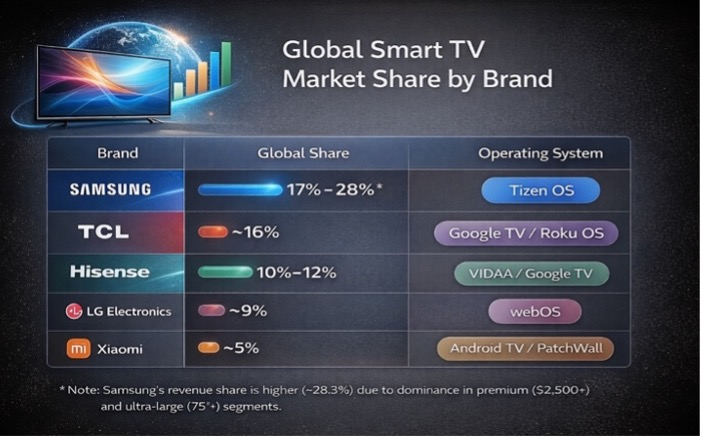

Global smart TV brand share (by unit shipments, late 2024/early 2025):

Key global trends: Android TV/Google TV is the fastest-growing OS segment (projected 5.9% CAGR), driven by adoption across Hisense, TCL, and Sony. Retailer-owned brands (e.g., Walmart/Vizio) now capture roughly 5% of global TV shipments—a 2025 inflection point where retailers control the OS to capture high-margin ad revenue.

US Market: Smart TV OS vs. Total CTV Device Share

The US Connected TV (CTV) ecosystem requires a critical structural distinction between:

- Smart TV OS Share → The operating system embedded in the television

- Total CTV Device Share → All access points, including Smart TVs, streaming sticks/boxes (Roku, Fire TV, Apple TV), gaming consoles (PlayStation, Xbox).

🔍 Why This Distinction Matters: The battle for CTV dominance is not won at the TV level—it is won at the access layer.

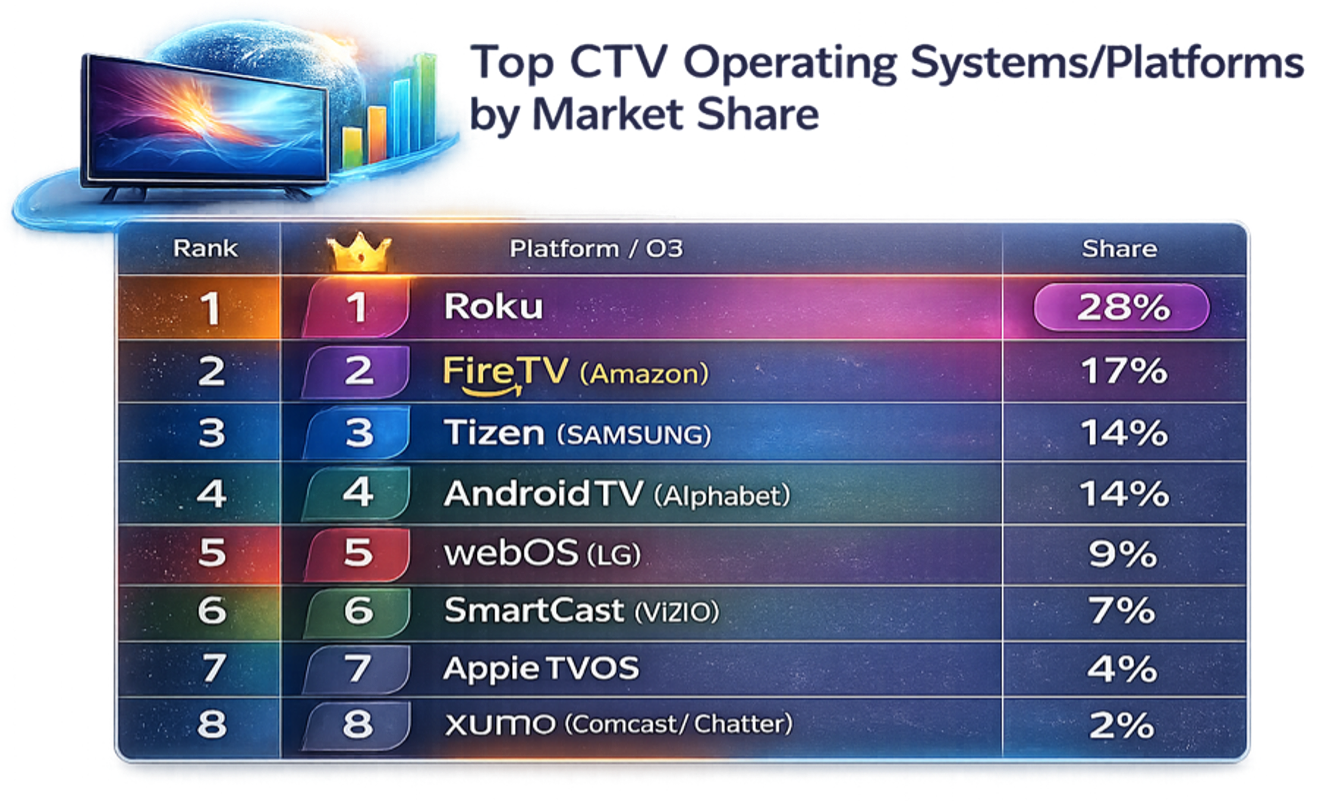

• Dominates total device share

• Embedded OS (OEM partnerships) + strong streaming device ecosystem

• Presence across both embedded + external layers → maximum reach

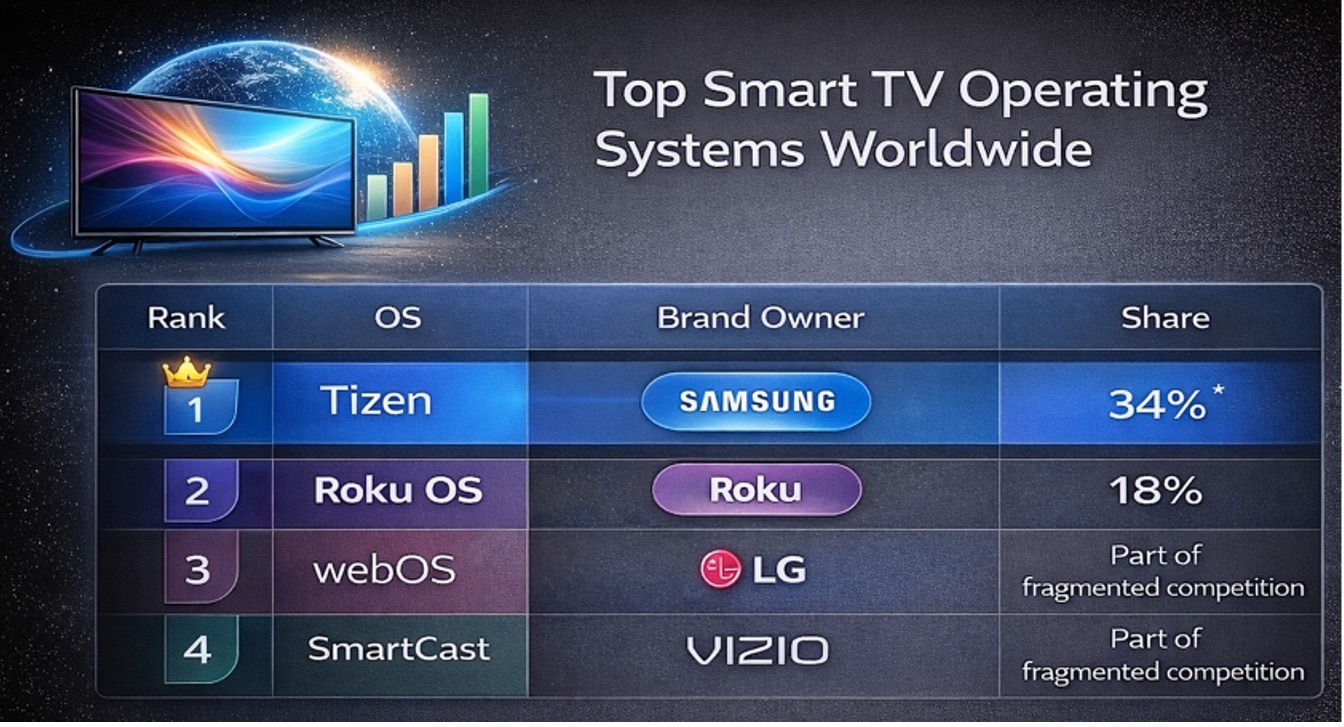

• Leads Smart TV OS share

• Premium TV dominance, global hardware scale

• Limitation: No meaningful presence in streaming sticks or external devices

• Strong in streaming devices and increasing OEM integrations

• Positioned between Roku and OEMs

📈 Growth Dynamics: Emerging Players

🚀 Xumo (Comcast / Charter): Fastest-growing platform (+64% YoY), backed by ISP distribution power and last-mile customer ownership. Its integration into broadband bundles and pay-TV transitions allows Comcast/Charter to reposition Xumo as the default CTV gateway for cord-cutters, not just another app ecosystem. Over time, this positions Xumo to control the UI layer, advertising inventory, and customer relationship, effectively blending telco and platform economics.

📊 Android TV (Google): ~10% YoY growth, driven by a global OEM ecosystem (Sony, TCL, Xiaomi) and deep integration with Google services (Search, YouTube, Assistant). Its strength lies in scale and flexibility, enabling rapid international expansion. However, a fragmented UX across OEM implementations limits consistency and monetization efficiency compared to Roku’s standardized interface and Amazon’s tightly controlled ecosystem, creating challenges in user engagement and advertiser value capture.

🧠 Strategic Implications

- Smart TV presence alone is insufficient

- Must optimize across:

- Embedded OS

- Streaming devices

- Content surfaces

- Roku wins because it exists everywhere the user can enter

- TV

- HDMI

- OS layer

- Samsung leads OS share

- But does not control access layer breadth

- Xumo signals a new model:

- Distribution + connectivity + platform

Distribution Strategy: The OS/Device Layer as a Strategic Control Point

The Paradigm Shift: From App-Centric to OS-Centric Behavior

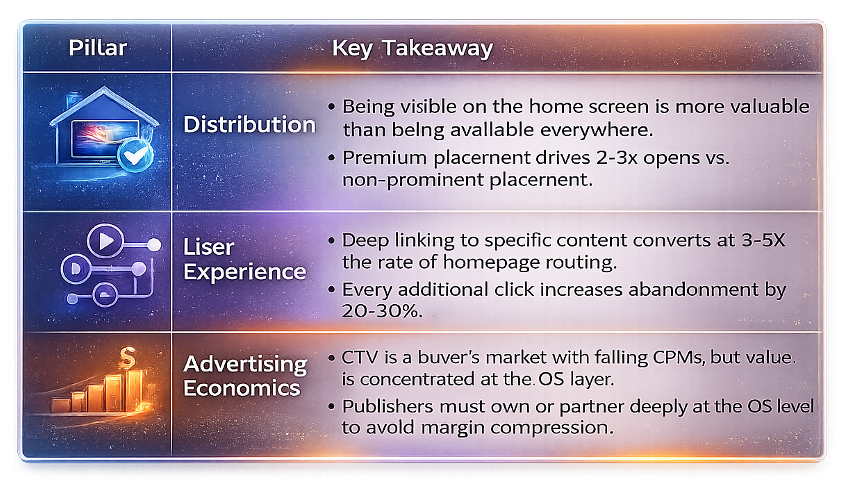

CTV environments operate as closed, platform-governed ecosystems where the OS is the primary orchestrator of user attention. Lean-back consumption, limited input mechanisms, and high reliance on algorithmic surfacing mean: "Installed but not surfaced" is functionally equivalent to "non-existent."

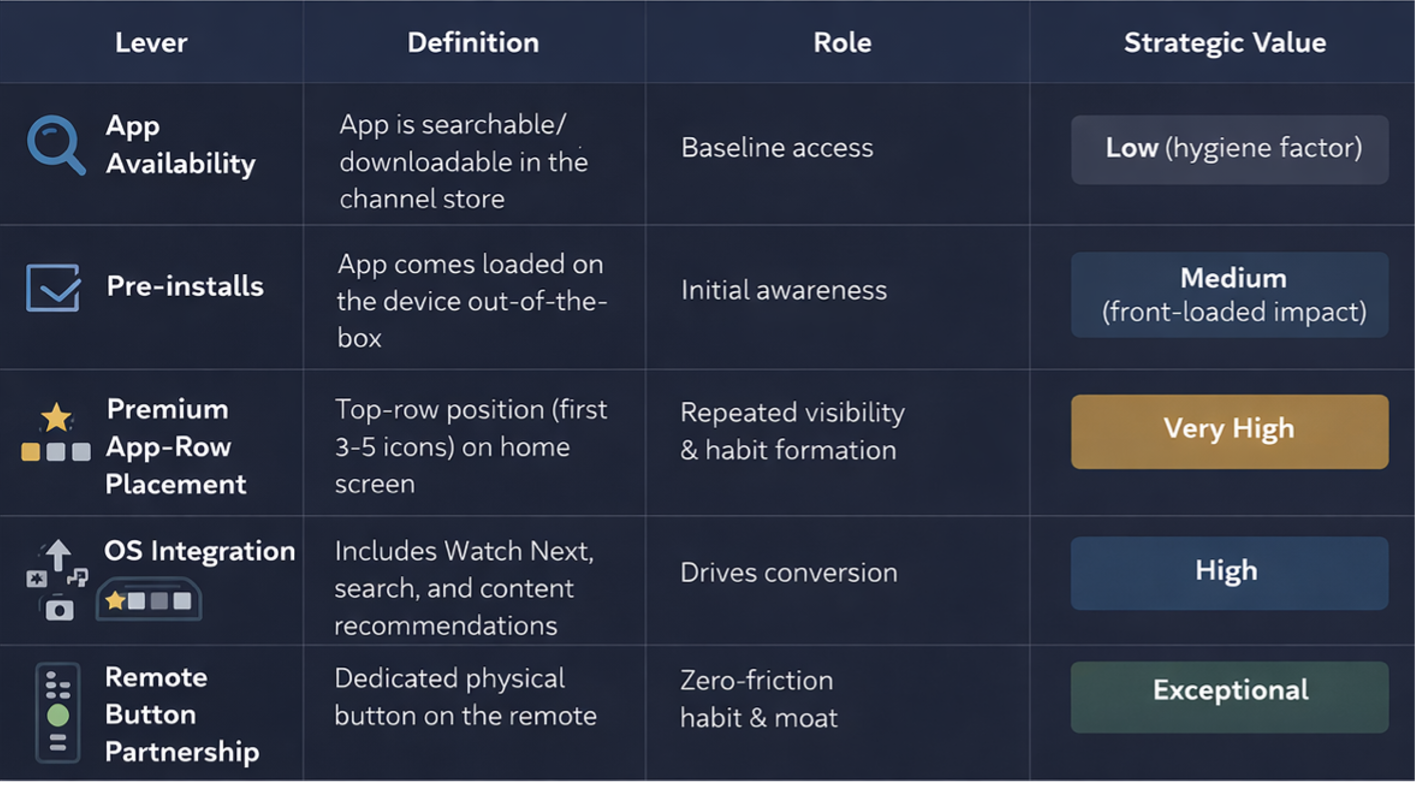

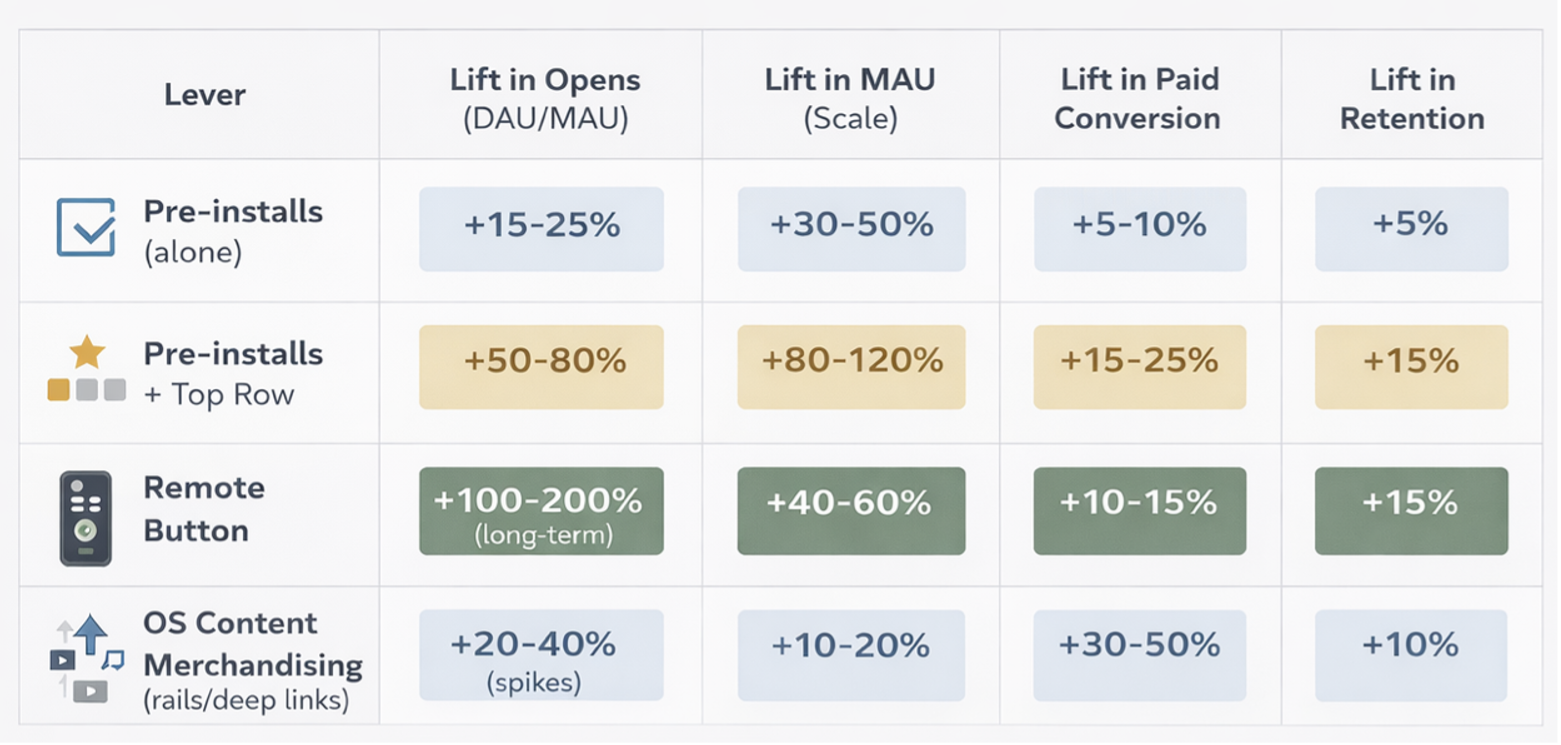

The Five Levers of CTV Distribution: A Hierarchical Framework

Key insight: Premium placement (top row) receives 70-80% of all home screen impressions. If your app is on row 2 or 3, it is effectively invisible.

Quantifying Incremental Lift by Lever

Strategic implications: For volume (MAU growth): prioritize pre-installs + premium row placement. For revenue (paid conversion): prioritize OS-level content merchandising and deep linking. For valuation (LTV/churn reduction): the remote button is the only lever that builds a sustainable habit.

Deep Linking: The Highest-Value Conversion Lever

Deep linking reduces time-to-play from ~45 seconds to ~5 seconds for live events. Users who click a deep link convert to paid subscribers at a rate 40% higher. Telcos can mandate deep-linking capabilities as part of distribution deals.

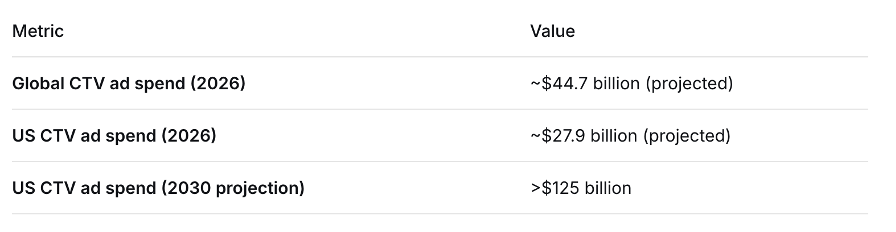

Advertising Economics: Growth, Structure, and Value Distribution

Market Size and Growth

Growth drivers: shift from linear TV to streaming, increasing ad-supported tier adoption, programmatic automation.

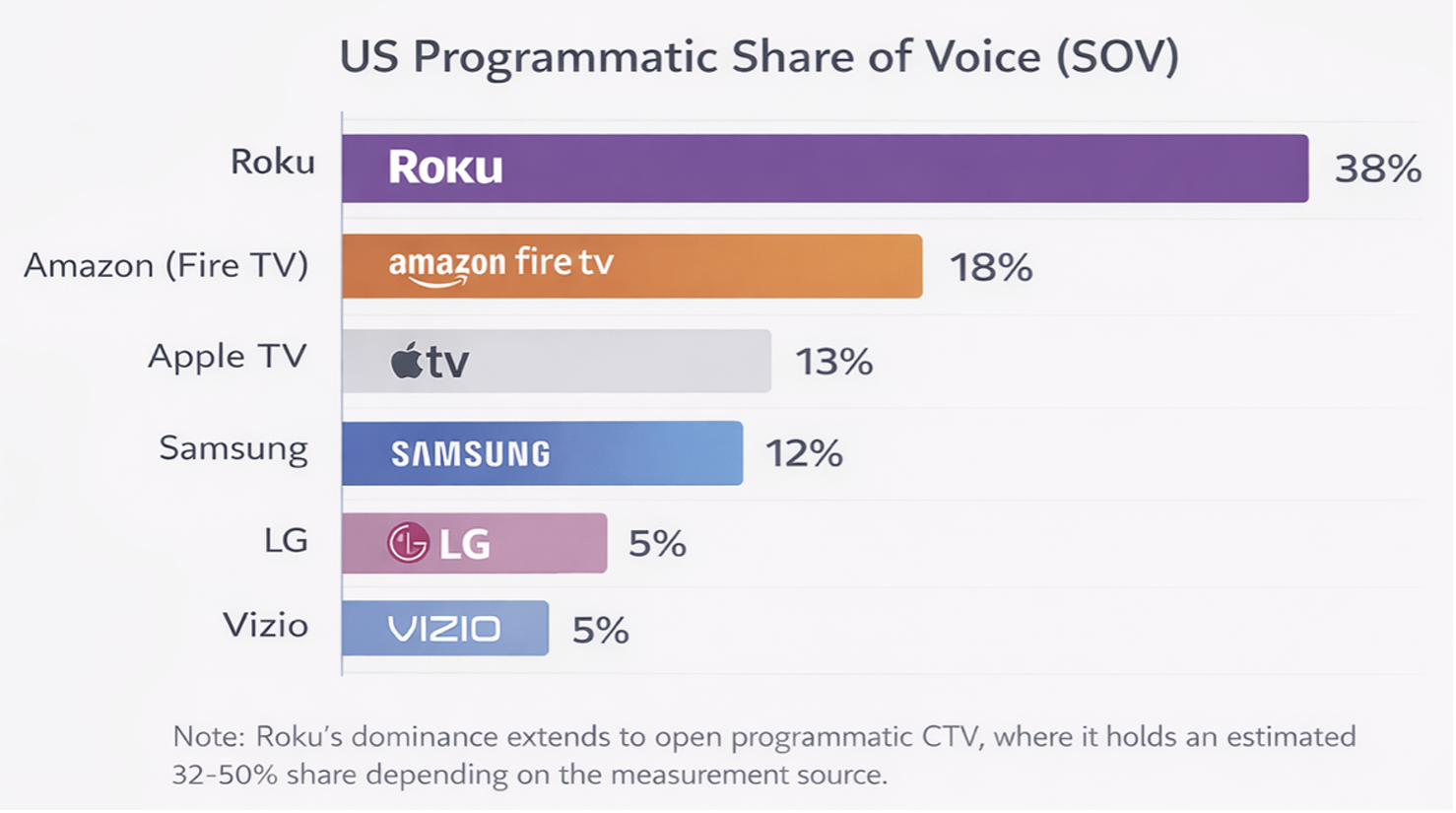

Competitive Landscape: Programmatic Ad Share (US)

CPM Trends: A Buyer's Market Emerges

Average CTV CPM (2025): ~$20-$25 (down from $30-$35 in 2022). Programmatic CTV CPMs often $15-$20. Premium inventory (live sports) still commands $35-$50+. Falling CPMs due to supply surge, ad load increases, buyer consolidation.

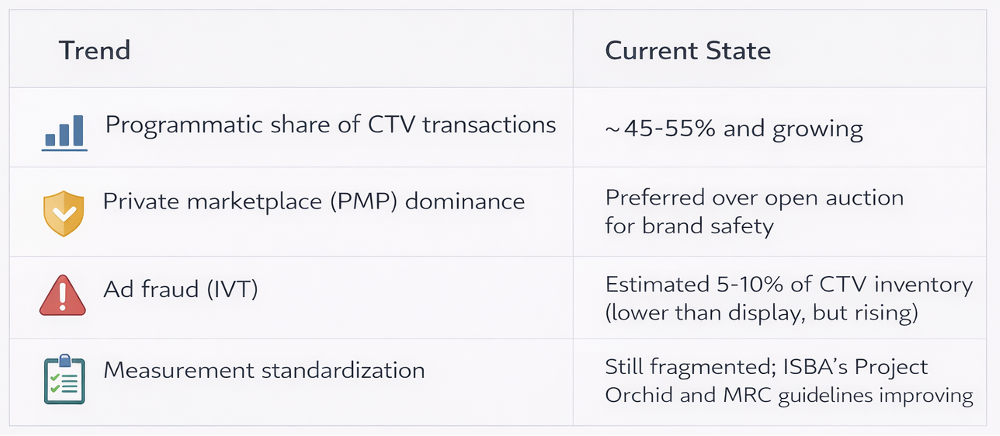

Programmatic Trends and Ad Fraud

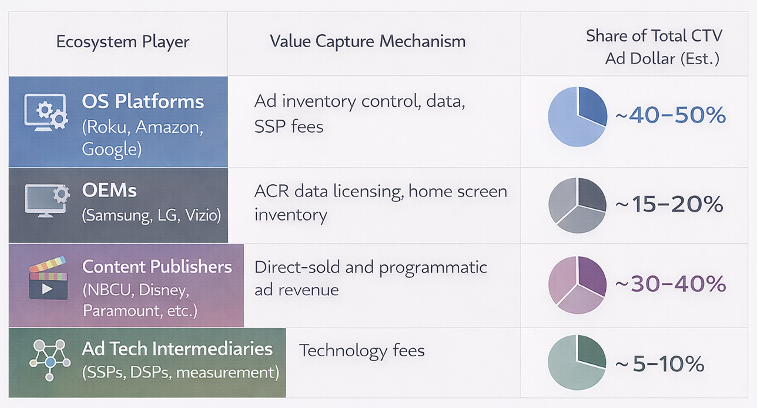

The Publisher Squeeze: Where Value Actually Accrues

Why publishers are squeezed: OS platforms control the home screen, ACR data advantage, revenue share requirements (15-30% of subscription revenue). Winning requires owning or partnering deeply at the OS layer.

Strategic Implications for Advertisers and Publishers

• Leverage falling CPMs

• Demand measurement rigor, avoid MFA inventory

• Prioritize platform-direct deals (Roku OneView, Amazon DSP, Google DV360)

• Use deep linking in ad creative (QR codes, companion ads)

• Invest in OS integration, not just distribution

• Use telco leverage if available

• Treat deep linking as a contractual requirement

• Consider OS ownership or deep partnership

Telcos have unique structural advantage: hardware distribution leverage, bundled billing, set-top box control.

Recommended baseline: pre-installs + premium row placement as minimum ROI driver, with the remote button as ultimate strategic asset.Conclusion: The Three Pillars of CTV Success

Winning in CTV is no longer about having the best content alone. It is about winning the moments before the app is even launched—through OS prominence, deep integration, and a distribution strategy that treats the platform as a strategic partner, not just a channel.

In the US CTV market, ownership of the television does not equate to ownership of the viewer. The true power lies with platforms that control multiple entry points into the ecosystem—making aggregation, not installation, the defining metric of dominance.

Based on Q1 2026 CTV device market research: Parks Associates CES 2026, S&P Global (Kagan), Antenna, Nielsen, Comscore. DOWNLOAD PDF VERSION